This would seem the perfect time for an Easter egg analogy.

Gather ’em up, put ’em in a basket.

And count ’em up.

Each one is a little unique, different from the others. But still an egg.

Last week, we began describing the concept of forecasting revenues and expenses. Let’s start with revenues.

For the sake of our egg analogy, we’re going to treat each of our revenue-generating projects as an egg. Large and small, beautiful or ugly, let’s identify them all, and yes– put them all in one basket. Then we can add ’em up.

It’s worth reminding ourselves at this point how to calculate Net Revenues. We only want to consider Net revenues for this exercise.

And we want to be sure we’re only counting our actual, real, revenue projects. No wishful thinking here. Just the hard reality of the projects for which we are already earning fees, or will begin doing so very soon based on a client agreement.

Once we’ve collected all of our eggs, we must break them open. We must break down the Net Revenues for each project into month-by-month amounts, representing what we will earn for each of those months.

If we don’t know, we need to find out. Uncertainty is the enemy of good forecasting. Someone in the firm knows the fees and the schedule. We need to find them, gather this information, and record it.

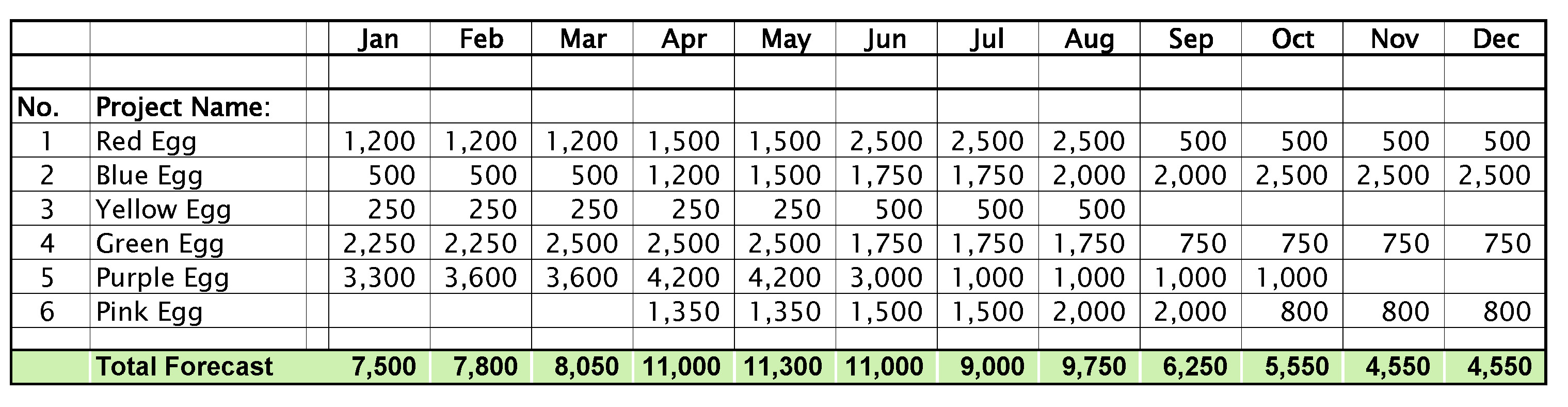

Here’s what we’re striving for:

So, there they are.

All our eggs in one basket.

Actually, we can separate them into separate baskets– for different offices, different practice studios, or different markets. We can do it in any way that helps us analyze our revenues.

The goal is to get to month-by-month totals for the whole basket. This constitutes a forecast, or revenue projection. Based on what we know today. It will certainly change tomorrow.

The following month, we can always update it, as the project fees, schedules, or teams change. And every month after that.

That’s all there is to it.

Happy Easter.

And may all your eggs be golden.