The fortune-teller peers into her crystal ball and claims to see the future. Who knows what she is really seeing, if she sees anything at all. Perhaps she is making up the story as she goes. If we could see the future for ourselves, she’d be out of business.

Let’s do that– let’s create a way to see our own future.

We just need our own crystal ball.

What we want is a reliable way to know what is going to happen in the near future, at least in terms of our firm’s profitability. A couple weeks ago, we said that we can do this with forecasting.

But, in order for us to succeed at reliable forecasting, or projection, we need to understand exactly what it is we are trying to predict.

First, we must establish a time period for which we are forecasting. While we can certainly forecast for any period we wish, the most logical approach is to forecast month by month, for the firm’s fiscal year, or whatever remains of our fiscal year. That way, we can compare our projection for the coming months with recent past months from our firm’s monthly Income Statements.

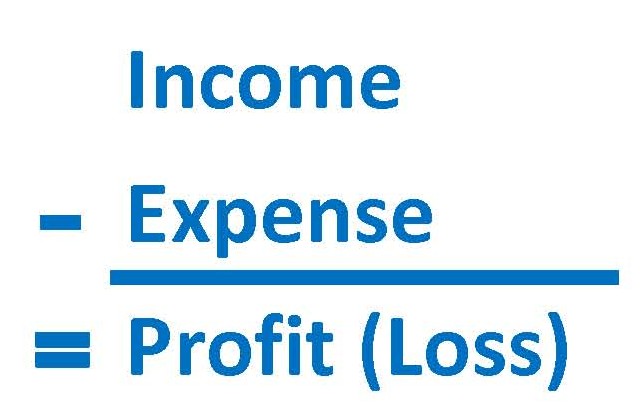

Second, we know that our Income Statement calculates profitability by breaking it down as follows:

Simple. All we need to do now is project our Income and our Expenses in order to predict profitability.

Our Expenses are easily forecasted, but must first be separated into Labor and Indirect Expenses. Labor is merely our salaries and wages paid to our staff. We know who they are, and what they are paid, so this is a very straightforward exercise. Indirect Expenses can be found itemized on our Income Statement. Projecting these costs into the near future is a fairly simple matter.

Projecting Income (revenues or fees), is a bit more of an art form. It requires a bit more diligence and discipline. Diligence to constantly track the various streams of revenues from all of our projects.

Just as important is the discipline to discern the difference between the real, going-to-happen, hard-reality revenues, and the hope-they-happen revenues. The latter should be considered Prospects until such time as they are truly real and going to happen for sure. We can’t take Prospect revenues to the bank.

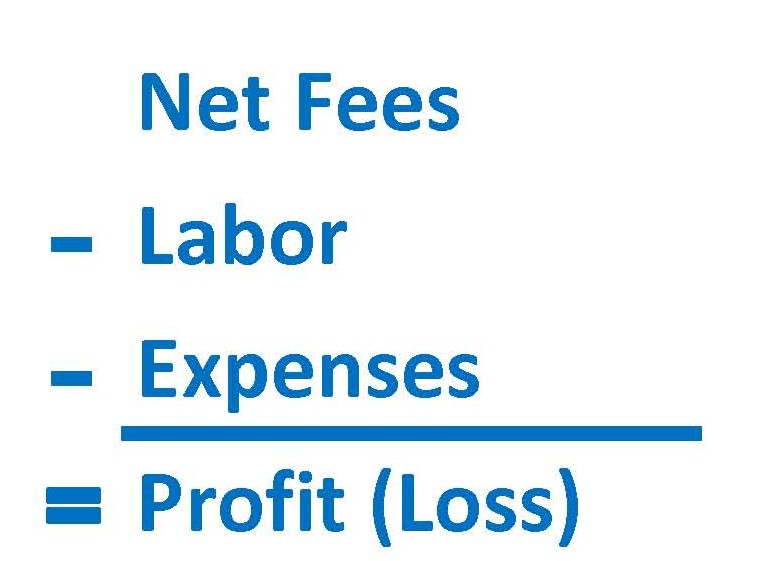

And we must be sure to focus on our Net Revenues. We already know that, to calculate Net Revenues from our Gross Revenues, we must subtract our consultants’ fees, as well as any billable (reimbursable) expenses.

So, to summarize, what we want to forecast, or project, are the components of the following equation:

If we simply forecast the first 3 elements, we can easily forecast our Profit Margin. We can take these one by one, and demonstrate how we can predict each of them in detail. After we’ve done it once, it’s fairly easy to keep it going.

Unlike the fortune-teller, who is only looking at the crystal ball when she has a customer, we must be continually looking to see what is coming.

The information is there for us.